Une offre très riche, un financement important, une audience plus forte que l’audiovisuel privé et un statut particulier — celui d’un audiovisuel de droit public (öffentlich-rechtlich) —, l’audiovisuel public allemand est né d’une histoire marquée notamment par la volonté des Alliés de rompre avec le système nazi, puis régulé par les jugements de la Cour constitutionnelle fédérale (Bundesverfassungsgericht), ainsi que par un rapport à l’État dans ses différentes acceptions (exécutif et parlements aussi bien de l’État fédéral que des Länder) et au politique bien plus étroit qu’on ne l’imagine.

Une organisation régionale

L’Allemagne connaît depuis la fin des années 1980 un système mixte dans lequel coexistent un audiovisuel privé et un audiovisuel public très largement régionalisé et qui relève de la compétence des Länder.

Les programmessont produits tout d’abord par des Rundfunkanstalten (instituts de l’audiovisuel) régionaux nés dans l’après-guerre

et regroupés depuis 1950 au sein de l’ARD (Arbeitsgemeinschaft der öffentlich-rechtlichen Rundfunkanstalten der Bundesrepublik Deutschland) ; ces neuf instituts, qui correspondent soit à un Land soit à une région plus vaste, produisent chacun entre trois et six programmes radio régionaux. L’offre de radio est traditionnellement régionale et ce n’est que depuis la réunification que l’Allemagne dispose de trois radios nationales publiques (Deutschlandfunk, DeutschlandradioKultur, DRadio wissen).

En ce qui concerne la télévision, les instituts réunis dans l’ARD produisent ensemble depuis 1952 le programme de la première chaîne (Das Erste), en contribuant chacun pour une quote-part des programmes (par exemple, le journal télévisé Tagesschau est produit par le NDR). Chaque institut produit également son programme régional ; ceux-ci sont réunis sous l’appellation Die Dritten Programme (« Les troisièmes programmes »). Enfin, l’ARD produit également les chaînes numériques Tagesschau24, Einsfestival et EinsPlus.

La deuxième chaîne de télévision, ZDF (Zweites Deutsches Fernsehen), est depuis 1963 produite de manière centralisée à Mainz, mais elle relève également des Länder ; nous reviendrons sur son histoire spécifique. Elle produit également les chaînes numériques ZDFneo, ZDFinfo, ZDFkultur. L’ARD et ZDF coopèrent pour les chaînes Phoenix et KiKA et participent aux programmes d’Arte et de la chaîne culturelle 3sat.

De Tatort à la Tagesschau : des émissions cultes

En ce qui concerne la radio, l’offre se composait en 2014 à 59 % de radios privées, 16 % de radios publiques et 25 % d’autres radios (associatives, confessionnelles etc.)

. Pourtant, en parts d’audience, les radios publiques sont loin devant avec 55 %, contre 43 % pour les radios privées. L’arrivée de la radio privée n’a donc pas bouleversé le paysage, ce qui s’explique par l’existence déjà ancienne d’une vaste gamme de radios publiques régionales.

Côté télévision, les chaînes publiques restent en tête des audiences : 13,3 % pour ZDF en 2014, suivi de Das Erste (12,5 %) et de RTL (10,3 %). Cependant, le public des chaînes publiques est de plus en plus âgé, et chez les 14-49 ans, les chiffres sont de 13,4 % pour RTL contre 7,5 % pour Das Erste et 7 % pour ZDF. Pour les Dritte Programme, la part d’audience respective se situe entre 1 et 2,7 %. Les « nouveaux Länder » sont cependant un cas à part et l’on y constate une nette préférence pour les programmes privés.

Les programmes pour lesquels l’audiovisuel public domine sont les émissions d’information, les grands talk-shows du soir à contenu politique et sociétal, ainsi que les fictions policières. Tatort, le film policier du dimanche soir produit à tour de rôle par les différents instituts de l’ARD, est une véritable institution dont la diffusion est abondamment commentée dans les autres médias et sur les réseaux sociaux. En ce qui concerne les informations télévisées, la télévision publique domine les audiences depuis plus de vingt ans, avec un écart net par rapport à ses concurrents privés, ce qui tient, entre autres, à la variété des formats (journaux télévisés, magazines, reportages). On trouve largement en tête cette autre institution qu’est la Tagesschau, le plus ancien journal télévisé allemand, et son édition principale diffusée de 20 heures à 20 h 15 sur Das Erste, Die Dritten, 3sat et Phoenix, avec 31,4 % de part d’audience, loin devant RTL aktuell sur RTL (16,9 %) et Heute sur ZDF (15,9 %) (chiffres 2012). La Tagesschau est caractérisée par un aspect austère et une réputation solide de sérieux et de fiabilité, au point que le changement de studio et le fait que, depuis octobre 2015, les présentateurs soient désormais visibles en pied a fait l’effet d’une révolution.

Une analyse précise des programmes télévisés pour 2014

montre que l’identité spécifique des chaînes publiques repose sur la part importante que l’information prend dans leurs programmes. Les chaînes privées se distinguent au contraire par la part plus importante accordée au « divertissement non-fictionnel » et, tout particulièrement, à la télé-réalité.

Un système mal aimé imposé par les Alliés occidentaux

Le système actuel est né après 1945 et après douze ans de dictature durant lesquels la radio mais aussi la télévision naissante ont été totalement mis au service de l’idéologie national-socialiste. L’audiovisuel public tel qu’on le connaît aujourd’hui en porte les traces, car les jalons posés après 1945 et le cadre réglementaire ont été élaborés par contraste avec cet audiovisuel totalement instrumentalisé. Mais même si la période nazie reste le contre-modèle permanent de la réflexion sur les médias en Allemagne, il ne faudrait pas en déduire une totale indépendance de l’audiovisuel public par rapport à l’État et aux partis politiques.

La période nazie reste le contre-modèle permanent de la réflexion sur les médias en Allemagne

Les Alliés occidentaux occupant l’Allemagne (1945-1949) souhaitaient rompre avec le système mis en place par les nazis et implanter un audiovisuel qui ne soit ni commercial ni d’État, mais de droit public et régional. Il s’agissait en particulier, dans le cadre d’une rééducation à la démocratie, d’éviter toute influence de l’État (État fédéral et Länder) sur les programmes et, ainsi, toute instrumentalisation par celui-ci, ce qui se heurta de front à la vision qu’avaient les politiques allemands pour qui l’audiovisuel devait relever, comme sous Weimar, de la responsabilité des organes de l’État. Les Alliés parvinrent certes à imposer leur modèle (porté notamment par Hugh Carlton Greene, futur directeur général de la BBC), mais la forme finale, entièrement nouvelle à l’époque et spécifiquement allemande, fut celle d’un compromis. Le contrôle ne devait pas être exercé par l’État mais par la société civile, représentée par des « groupes importants pour la société » (gesellschaftlich relevante Gruppen). C’est justement dans la désignation de ces groupes que s’exprima la résistance des politiques allemands, très motivés pour essayer de faire rentrer l’État malgré tout dans les instances de l’audiovisuel public. Wördehoff parle très justement d’un « défaut de naissance de l’audiovisuel public, celui d’être un enfant non désiré de la démocratie allemande, mal aimé, adopté de force (…)»

.

La Loi fondamentale de 1949 établit dans son article 5 le principe de Rundfunkfreiheit (liberté de l’audiovisuel) et les médias relèvent de la compétence législative des Länder, qui adoptèrent des lois sur les médias à peu près similaires en organisant les différents instituts de manière identique. Ceux-ci sont des instituts d’intérêt public et de droit public autonomes, qui s’administrent eux-mêmes. Ils ont un Rundfunkrat (« conseil de l’audiovisuel ») qui doit contrôler que la mission attribuée aux instituts quant aux programmes est respectée. Ses membres émanent des groupes « importants pour la société », dont la liste est fixée par les lois sur l’audiovisuel des Länder respectifs. Le Rundfunkrat élit l’Intendant, le directeur, qui n’est donc pas désigné par les instances de l’État. Enfin, le Verwaltungsrat (conseil d’administration) a pour mission principale de conseiller l’intendant quant aux questions financières et de surveiller la gestion.

L’Allemagne semble donc, sur le papier, relever du type « démocratique-corporatiste » caractéristique de l’Europe du Nord dans lequel, selon Hallin et Mancini, le contrôle est attribué aux partis politiques et « groupes importants pour la société ». Toutefois, la réalité est plus nuancée, en particulier dans les instituts fondés le plus tardivement, après que les Allemands eurent récupéré en 1955 la souveraineté quant à l’audiovisuel, qui sont aussi ceux où l’Etat est le plus présent.

Des missions de service public fixées par les juges constitutionnels

Le chancelier Adenauer, pour sa part, rêvait d’une loi qui aurait permis d’établir une mainmise de l’État fédéral sur l’audiovisuel public. Cela se traduisit en 1960 par la tentative de fonder une deuxième chaîne de télévision, à la fois nationale, privée et contrôlée par l’État fédéral, ce qui valut au projet le surnom de « télévision Adenauer ». Plusieurs Länder dirigés par le SPD portèrent alors plainte devant le Bundesverfassungsgericht, ce qui donna lieu en 1961 au premier jugement sur l’audiovisuel qui a depuis acquis le statut d’une sorte de Loi fondamentale dans ce domaine. D’ailleurs, le droit des médias allemand est en grande partie écrit par les juges constitutionnels. Ce jugement fixe deux principes importants la compétence exclusive des Länder en ce qui concerne la législation sur l’audiovisuel et l’obligation de Staatsfreiheit (« liberté par rapport à l’État ») ou de Staatsferne (« distance par rapport à l’État ») pour l’audiovisuel public. Ce jugement interdisant la « télévision Adenauer », ce sont les Länder qui créeront en 1961/1962 la deuxième chaîne de télévision (ZDF, Zweites Deutsches Fernsehen).

Selon le Bundesverfassungsgericht, il faut protéger l’audiovisuel, qui est à la fois un « média » et un « facteur » dans la formation de l’opinion publique, d’une influence « dominante » de l’État. L’État (c’est-à-dire les « États-régions» que sont les Länder) a cependant l’obligation de promulguer des lois qui organisent l’audiovisuel public, garantissent le pluralisme et définissent les missions respectives des instituts. Ce point de vue et, plus généralement, le rôle de l’audiovisuel public dans la société démocratique ont été développés dans les jugements suivants.

Le passage à un système mixte a également été préparé par des arrêts du Bundesverfassungsgericht, pour aboutir à un arrêt de novembre 1986 qui a définitivement ouvert la voie à l’existence de l’audiovisuel privé, tout en définissant les missions du secteur public par la notion de Grundversorgung (« service de base », à ne pas confondre avec un « service minimum ») : cette mission de l’audiovisuel public comprend l’accès de tous à la réception des programmes, la garantie de standards en ce qui concerne les contenus et la garantie du pluralisme par le pluralisme interne de la composition des conseils. On exige donc de l’audiovisuel public ce que l’audiovisuel privé, soumis aux lois du marché, ne peut ou ne veut pas fournir. Ce devoir implique également que l’audiovisuel public doit voir son existence et son fonctionnement garantis en ce qui concerne les équipements techniques, l’organisation, les personnels et les finances. C’est suite à cet arrêt que les Länder signèrent en 1987 le premier traité interétatique sur l’audiovisuel (Staatsvertrag), maintes fois modifié depuis mais qui reste le cadre réglementaire du système mixte. Après la réunification, les nouveaux Länder de l'ex-RDA (dans laquelle l'audiovisuel était directement contrôlé par l'État selon le modèle soviétique) signèrent à leur tour ce traité, scellant la disparition des chaînes et radios de RDA et créant de nouveaux instituts d'audiovisuel public selon le modèle de l'Ouest qui devinrent à leur tour membres de l'ARD.

L’audiovisuel public voit donc son existence, tout particulièrement financière, garantie et a, en contrepartie, un certain nombre de missions à remplir en termes de programmes. Ceci a encore été confirmé par un arrêt du Bundesverfassungsgericht de mars 2014 : l’audiovisuel public doit être un contrepoids aux programmes privés et produire une offre qui suive une autre rationalité que celle du marché. « Sa mission ne se limite donc pas à un service minimum ou à combler des lacunes et des niches qui ne sont pas remplies par les programmes privés ; elle couvre l’ensemble de la mission classique de l’audiovisuel qui, à côté de son rôle dans la formation de l’opinion et de la volonté, à côté du divertissement et de l’information, comprend aussi une responsabilité culturelle et s’adresse à l’ensemble du public » (§37 de l’arrêt).

Un financement public mais indépendant de l’État

L’audiovisuel public se finance très majoritairement par la redevance et, dans une bien moindre mesure, par la publicité. Pour garantir la « distance par rapport à l’État » (Staatsferne), son financement ne peut se faire par le budget de l’État et passe par la redevance, qui est une taxe ciblée, et non par l’impôt. Le montant de la redevance est fixé par une procédure complexe qui se déroule en trois étapes depuis un arrêt du Bundesverfassungsgericht de 1994. Les instituts régionaux déclarent leurs besoins financiers pour les quatre années à venir sur la base des décisions prises en matière de programmes ; la KEF (Kommission zur Ermittlung des Finanzbedarfs derRundfunkanstalten, commission indépendante composée de seize experts nommés par les ministres-présidents des Länder) examine cette demande, puis transmet une recommandation aux gouvernements des Länder qui fixent ensemble le montant de la redevance, qui doit être validé par les différents parlements régionaux et donne lieu ensuite à un traité interétatique

.

Cette procédure a, elle aussi, donné lieu en 2007 à un nouvel arrêt du Bundesverfassungsgericht, après que les Länder eurent fixé en 2004 pour les quatre ans suivants un montant de la redevance inférieur à celui recommandé par la KEF, en arguant que les instituts devaient faire des économies en revoyant leurs programmes. Le Bundesverfassungsgericht a jugé que cette décision n’était pas recevable car elle empiétait sur l’autonomie de programmes de l’audiovisuel public et portait ainsi atteinte à sa liberté par rapport à l’État. Pour le Bundesverfassungsgericht, garantir la liberté de l’audiovisuel passe par assurer son fonctionnement, ce qui inclut un financement à la hauteur des besoins, et les instituts doivent être libres de choisir la manière dont ils remplissent les fonctions que leur attribue la loi.

Réforme de la redevance et hausse des recettes

Le système de perception de la redevance a changé en 2013 pour passer du modèle de la Rundfunkgebühr, taxe liée au nombre d’appareils, au Rundfunkbeitrag, contribution à l’audiovisuel qui concerne tous les foyers et entreprises. Le but de la réforme était de régler la question de savoir s’il fallait taxer la propriété de terminaux connectés permettant de consommer radio et télévision. Le principe est que l’on paie non pas pour l’utilisation des programmes de l’audiovisuel public, mais pour l’existence même de ces programmes et la possibilité de les utiliser.

Cette contribution est due à la fois par les particuliers (qui représentaient en 2012 91 % des recettes) et par les entreprises, avec des seuils en fonction du nombre d’employés. De nombreuses institutions, comme des écoles, universités, églises, sont désormais également concernées et la réforme a diminué le nombre de réductions et exonérations possibles. Cela a eu pour conséquence, d’après l’estimation de la KEF, une hausse des recettes de 1,16 milliard pour la période 2013-2016. En conséquence, le montant de la redevance a été abaissé de 17,98 euros à 17,5 euros mensuels au 1er avril 2015, un montant qui reste élevé mais qu’il faut rapporter à la taille de l’offre de programmes.

Un des principaux opposants à cette réforme est le loueur de voitures Sixt, qui doit dorénavant payer une redevance pour chacune des agences et de ses véhicules. Ses plaintes ont jusqu’ici été rejetées par différents tribunaux administratifs bavarois, et Sixt compte aller désormais devant le Bundesverfassungsgericht.

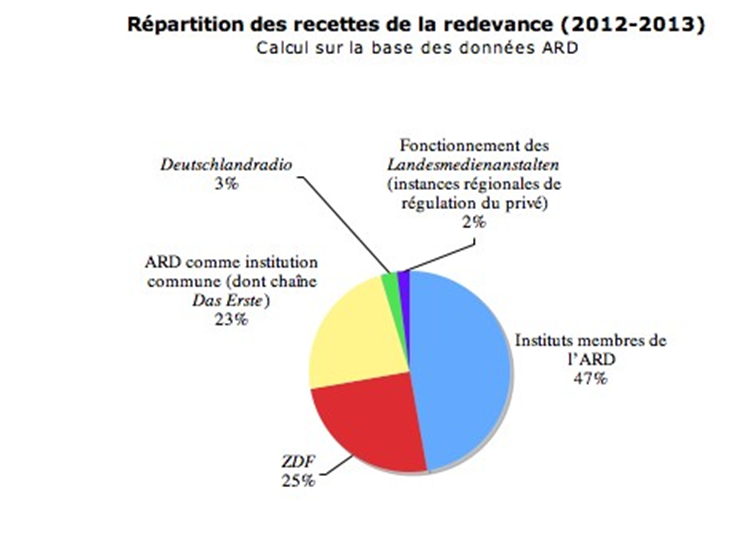

Les recettes de la redevance sont réparties entre les différents acteurs de l’audiovisuel public comme le montre le graphique ci-dessous.

Crédits : Valérie Robert.

La part de la redevance dans les recettes se situe entre 83 % (ZDF, 2013) et 85 % (ARD, 2014), celle de la publicité et du sponsoring entre 6 % (ARD, 2014) et 6,8 %

Le lobby de l’audiovisuel privé réclame pour sa part une réduction voire à long terme une interdiction de la publicité pour l’audiovisuel public.

Une autonomie garantie par la constitution mais en trompe-l’œil

Que le Bundesverfassungsgericht ait eu besoin de statuer à de nombreuses reprises sur la question du rapport à l’État montre que la « distance par rapport à l’État » (Staatsferne) n’est pas toujours respectée. L’influence de l’État passe, par exemple, dans les conseils des instituts, par une forte présence de députés régionaux, de ministres-présidents ou de représentants de la société civile désignés par les parlements ou gouvernements régionaux. Jusqu’en 2015, dans le conseil d’administration de la ZDF, les représentants directs de l’État (dont plusieurs ministres-présidents) pouvaient ainsi, grâce aux règles de majorité, exercer une influence sur les programmes.

On assiste également à un partage du pouvoir entre grands partis (CDU/CSU et SPD), représentés dans les conseils de manière directe, mais aussi de manière camouflée par les représentants des groupes sociaux, notamment lorsque ceux-ci sont également membres de partis politiques. Ils dominent également les débats dans les conseils par le biais de « cercles d’amis » (Freundeskreise) qui fonctionnent selon le modèle de groupes parlementaires, préparent les votes et à l’emprise desquels il est difficile de se soustraire.

Les partis ont toujours cherché à instrumentaliser l’audiovisuel

Leur domination commune repose également sur un système officieux de partage des postes, le Proporz, une sorte de grande coalition permanente. La répartition des postes fait l’objet d’un accord tacite et se fait non pas chaîne par chaîne, comme dans le système italien de lottizzazione, mais niveau par niveau à l’intérieur du même institut. Les partis se mettent d’accord sur des Personalpakete (« tickets ») : ainsi, à la ZDF, l’intendant est traditionnellement « noir » (CDU/CSU), le rédacteur en chef « rouge » (SPD), le directeur des programmes « noir », etc. La politique de recrutement est une politique des programmes en amont, et les partis ont toujours cherché à instrumentaliser l’audiovisuel.

Parmi les nombreux exemples d’intervention politique, la plus visible — et celle qui a mis en lumière un problème structurel — a été lorsqu’en 2009, le conseil d’administration de la ZDF a refusé de renouveler le contrat du rédacteur en chef, un vote organisé par le ministre-président CDU de Hesse, qui siégeait au conseil d’administration avec quatre autres ministres-présidents et un ministre fédéral. Le scandale a été tel que, après maintes tergiversations – et sous la pression publique des journalistes, de juristes mais aussi de petits partis rivaux — plusieurs Länder SPD ont déposé en 2010 un recours auprès du Bundesverfassungsgericht. Un niveau de l’État, celui des Länder, a donc été contraint de demander l’examen de la légalité de l’influence conjointe des grands partis et de l’État… L’arrêt du 25 mars 2014 a effectivement conclu au caractère non constitutionnel de la composition des conseils de la ZDF, mais aussi d’autres instituts, et stipulé que, si la présence en leur sein des différents niveaux de l’État n’est pas exclue, leur composition doit également obéir au principe de Staatsferne

. Pour éviter une instrumentalisation politique de l’audiovisuel, il faut donc limiter l’influence des membres représentant l’État ou proches de celui-ci à un tiers maximum des membres. De plus, l’exécutif ne doit pas avoir d’influence déterminante sur le choix des autres membres, et il faut prévoir des clauses d’incompatibilité. Un des juges a insisté sur le fait que, pour lui, cet arrêt n’allait pas assez loin, en particulier parce qu’il ne condamnait pas l’existence des Freundeskreise (« cercles d’amis »).

Pour autant, la représentation d’un audiovisuel public indépendant de l’État reste dominante en Allemagne ; elle semble avoir une fonction identitaire pour une démocratie qui tient à se démarquer en permanence du régime précédent. Des systèmes étrangers (la France mais, surtout, l’Italie) ont dans ce discours une fonction de repoussoir, ce qui implique de passer sous silence des ressemblances qui pourtant existent mais remettraient en question le mythe de l’indépendance. Ainsi, la presse allemande use et abuse du terme Staatsrundfunk (« audiovisuel d’État ») et de ses variantes pour désigner l’audiovisuel public de nombreux pays du monde (dont la France), sauf celui de l’Allemagne…

Haro sur le mastodonte ?

Cette vision positive coexiste cependant avec de nombreuses critiques qui ont en commun de vouloir au minimum réduire le financement et la voilure de l’audiovisuel public, au maximum de le supprimer. Ainsi, l’audiovisuel privé souhaite une suppression de la publicité sur les chaînes publiques, et critique par ailleurs l’expansion de l’audiovisuel public, notamment sur Internet (par exemple, un projet de chaîne en ligne de l’ARD et de la ZDF pour un public jeune). La presse de tendance néolibérale (notamment les quotidiens suprarégionaux Frankfurter Allgemeine et Handelsblatt) est très active contre l’existence même du « mastodonte » et son financement par la redevance. Cette position est notamment liée aux intérêts spécifiques de la presse quotidienne. Une modification de 2009 du traité interétatique sur l’audiovisuel Staatsvertrag a fixé que les sites internet des instituts de l’audiovisuel public ne peuvent être presseähnlich (assimilables à de la presse) que s’ils accompagnent une émission. Les éditeurs de presse avaient accusé les chaînes publiques d’outrepasser leur domaine d’activité en étant présentes sur Internet avec des sites gratuits financés par la redevance et qu’ils considèrent comme une concurrence déloyale. Par ailleurs,huit éditeurs ont porté plainte en juin 2011 contre ce qui est pour eux un produit assimilable à de la presse et l’information à ce sujet dans leurs journaux est loin d’être neutre. Après différents épisodes juridiques, la cour fédérale de justice a autorisé en avril 2015 un nouvel examen de leur plainte.

Mastodonte surfinancé ou service d’intérêt général indispensable, les points de vue divergent, et au bout du compte, ce sera probablement une fois de plus le Bundesverfassungsgericht qui devra un jour trancher cette question, peut-être, ce qu’espèrent les critiques, en réexaminant la notion de Grundversorgung qui, pour le moment, garantit l’existence plutôt confortable de l’audiovisuel public allemand.

[La suite du texte est une mise à jour, le 25/01/2017] La fin 2017 a vu l’audiovisuel public sur la sellette, attaqué par la presse et certains partis politiques, parallèlement à une renégociation par les Länder du Rundfunkstaatsvertrag (Traité interétatique sur l’audiovisuel).

Financement et redevance

Les Länder ont demandé aux instituts de l’audiovisuel public de présenter un plan d’économies structurelles ; un projet allant dans ce sens a été soumis fin septembre, il comporte en particulier des mutualisations dans le domaine administratif et technique. Mais c’est surtout la redevance qui fait parler d’elle : si l’audiovisuel public reste une référence en termes d’information et de crédibilité (en 2016, 75 % des personnes interrogées le trouvaient très ou plutôt crédible, 74 % selon une enquête du WDR), la redevance universelle est par contre très critiquée ; dans un sondage de février 2016, 70 % des personnes interrogées étaient favorables à sa suppression.

Après de nombreuses plaintes auprès des tribunaux, c’est maintenant au tour à la fois de la Cour constitutionnelle fédérale et de la Cour de justice de l’Union européenne de se prononcer, cette dernière devant examiner s’il ne s’agit pas d’une subvention qui nécessiterait alors une autorisation de la Commission européenne. La Cour constitutionnelle devrait auditionner les parties au printemps 2018 et se prononcer quelques mois plus tard.

La polémique autour des activités en ligne

La discussion porte également sur les possibilités et les limites de la présence en ligne de l’audiovisuel public, avec en arrière-plan son rôle dans l’information de l’ensemble de la population.

Actuellement, les émissions télé et radio ne sont disponibles en ligne que 7 jours, avec cependant des exceptions possibles. Les Länder discutent de la possibilité d’assouplir cette règle qui entame l’image de l’audiovisuel public, puisque les spectateurs ont l’impression d’avoir payé, par la redevance, pour des contenus qu’ils ne peuvent ensuite pas consulter indéfiniment en ligne.

L’audiovisuel public a par ailleurs beaucoup développé son offre en ligne. Du point de vue des éditeurs de presse, ceci constitue une concurrence déloyale car gratuite et ressemblant, à leur avis, trop à de la presse (« presseähnlich »). C’est autour de ce terme, anachronique et pas adapté aux problèmes actuels que se joue le conflit, alors même que dans l’autre sens, les contenus des sites des éditeurs se rapprochent de plus en plus de l’audiovisuel (vidéos, podcasts). Les éditeurs prônent pour leur part un modèle dans lequel la part des textes sur les sites de l’audiovisuel public serait réduite à 30 % des contenus. Certains instituts ont d’ailleurs déjà réduit la part de textes, comme par exemple le ZDF, le WDR ou Radio Bremen.

La polémique qui s’est développée dans la presse se caractérise par son caractère démesuré : en effet, sur un temps quotidien moyen passé en ligne de 45 minutes, 7 sont consacrées à lire des articles et la part de marché online de l’audiovisuel allemand est beaucoup moins élevée que sa part d’audience offline.

Cela pose la question de savoir si l’audiovisuel public est vraiment responsable des difficultés financières de la presse ou si celle-ci n’est pas davantage menacée par les GAFA. Quoi qu’il en soit, la presse allemande a transformé un problème économique en un combat dans lequel tous les coups sont permis, et où la disqualification du concurrent passe par l’utilisation de termes à connotation extrêmement péjorative comme « Staatspresse » voire une comparaison avec la Corée du Nord. Ceci sous-entend que l’audiovisuel public serait à la botte de l’État et que la presse, indépendante de l’État, serait, elle, guidée uniquement par le souci de l’information neutre – alors que dans ce cas précis, l’information y est mise au service d’un lobbying pour ses propres intérêts économiques, comme lorsque le Spiegel a consacré, le 7 octobre 2017, sa Une à cette « inquiétant pouvoir ».

Des attaques politiques

Les attaques contre l’audiovisuel public allemand s’inscrivent aussi plus largement dans un contexte politique spécifique. Si le parti libéral FDP a évoqué la possibilité de privatiser le ZDF, le parti d’extrême-droite AfD, qui a obtenu 12,6 % des voix aux dernières élections au Bundestag, se montre plus radical envers les médias « établis », qui constituent à ses yeux une « Lügenpresse » (« presse mensongère »), y compris l’audiovisuel public. La redevance est, elle, désignée comme un « Zwangsbeitrag », un terme très péjoratif que l’on pourrait traduire par « contribution imposée ». Dans son programme, l’AfD prévoit de changer le système de la redevance, de privatiser l’ARD et le ZDF et de mettre en place deux instituts plus petits, financés par des impôts (ce que la redevance n’est pas) et directement dépendants de l’État.

C’est d’ailleurs dans les Länder de l’Est, où l’AfD a obtenu le plus de voix lors des dernières élections législatives, que les gouvernements respectifs évoquent le plus une possible réduction de l’audiovisuel public…

Références

Konrad DUSSEL, Deutsche Rundfunkgeschichte. 2., überarbeitete Auflage, Konstanz, UVK, 2004.

Bernhard FRYE, Die Staatsaufsicht über die öffentlich-rechtlichen Rundfunkanstalten, Berlin, Duncker & Humblot, 2001.

Daniel C. HALLIN, Paolo MANCINI, Comparing Media Systems. Three Models of Media and Politics. Cambridge, Cambridge University Press, 2004.

Peter J. HUMPHREYS, Mass Media and Media Policy in Western Europe, Manchester / New York, Manchester University Press, 1996.

Karol JAKUBOWICZ, « Public Service Broadcasting: Product (and Victim?) of Public Policy », in Mansell, Robin / Raboy, Marc (Ed.) (2011a), The Handbook of Global Media and Communication Policy, Chichester, Blackwell, p. 210-229, 2011.

Valérie ROBERT, (2013a), « Staatsfreiheit ou intervention de l’État ? Le modèle allemand de l’audiovisuel public », in : Sur le journalisme, Vol. 2, N°2, 2013.

Heinz-Werner STUIBER, Medien in Deutschland., Konstanz, UVK, 1998.

--

Crédits photos :

ZDF Auslandstudios. Christian Scholz / Flickr

À lire également dans le dossier « Qu’est-ce qu’un média de service public ? » :

Quelles ambitions pour l’audiovisuel public français ?

Radio et TV en Pologne, du communisme aux médias de service public

L’audiovisuel public marocain, à la croisée des chemins ?

États-Unis : médias publics et financements semi-privés

Les médias audiovisuels publics au Brésil : un défi démocratique

Israël : l’audiovisuel public renaîtra-t-il de ses cendres ?

Les défis de la radio-télévision publique du Sénégal

Nigeria : des médias de service public plus nécessaires que jamais

L’audiovisuel public en Inde : des médias de gouvernement ?

NHK : au service du public ou du gouvernement japonais ?

L’audiovisuel public sud-coréen : un capital sympathie qui s’effrite

La BBC : un modèle de service audiovisuel public en danger